Not paying NZ Super out to those on incomes of $100,000 or more would save taxpayers around $608 million. Is it time we shake up who gets paid and what? RNZ‘s Nita Blake-Persen reports.

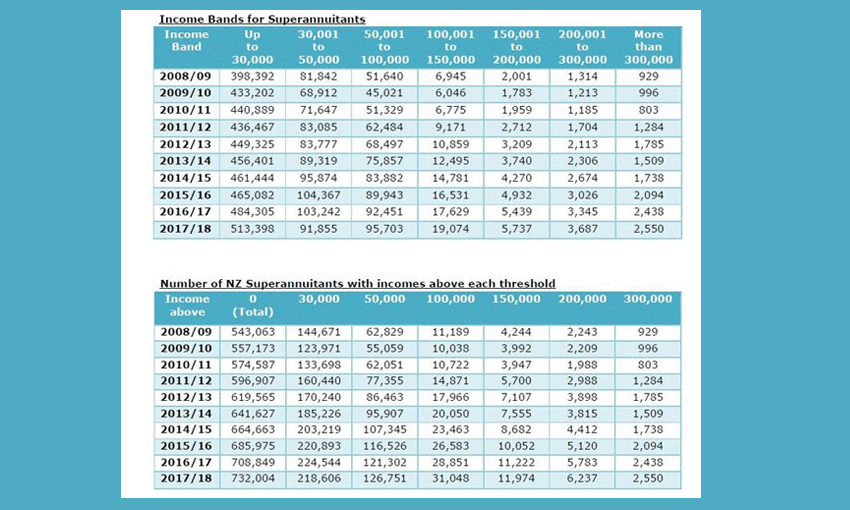

The number of New Zealand retirees getting their superannuation while earning more than $100,000 has topped 30,000, costing taxpayers more than half a billion dollars each year.

Figures released to RNZ’s Checkpoint show that number has nearly tripled over the past ten years and doesn’t even include incomes through Kiwisaver, or other investment portfolios.

Some economists say the numbers support means testing or income testing pension payments, but others say that risks throwing the baby out with the bathwater, and it’s vital Super remains universal.

The median New Zealand wage is nearly $53,000 and the number of Kiwis who are earning double that in their retirement ($100,000 or more) is more than 31,000. That’s roughly the population of Blenheim.

The latest Inland Revenue figures from the 2017/2018 financial year show that number is rising steadily – it’s nearly tripled since 2009.

Retirement Policy and Research Centre director Susan St John said the numbers were really an underestimate.

“It doesn’t count PIE (portfolio-investment entity) income and it also, of course, doesn’t count the capital gains many in those brackets will have enjoyed.”

Superannuation payments are universal in New Zealand and superannuitants make up the largest group of beneficiaries in the country.

There’s been much debate in recent years over whether to increase the current retirement age of 65 to reflect the fact people are working longer, but last month the interim retirement commissioner poured cold water on the idea of raising the age for Super, saying the current cost was sustainable for the next 30 years.

But St John said hard decisions needed to be made about the cost of NZ Super and whether there were better uses for that money.

“I think that increasingly the younger generation is looking sideways at the older population and seeing that they have had all kinds of advantages that are not enjoyed by younger people.”

Economist Shamubeel Eaqub said the figures weren’t surprising because a lot of people were continuing to work later in life and many had accumulated large amounts of wealth. He wanted Super to be means tested (related to wealth and income).

“The reality is that we don’t want to penalise people for working into old age and neither do we want to penalise people for accumulating wealth, but we have to be consistent in our understanding that actually when we look out to the next 20 to 30 years, our system of taxation and our systems of supporting old age and superannuitants probably isn’t sustainable.”

He said based on the current fiscal year, and on the average Super payment being $19,592, not paying it to people on incomes of $100,000 or above would save taxpayers around $608m.

“One day we’re going to wake up and realise we’re spending significant sums of our taxes on looking after folk who quite often will be pretty well off and don’t need the support.

“In those instances I think we’re going to have the necessary conversation about who gets to have access to New Zealand Super, at what level, and is universal Super something we can continue at the same time as wanting to do everything else, like deal with child poverty.”

St John had different ideas. She favoured a universal grant at 65 paid at the net rate of national super, but higher tax rates for those earning extra money through working or their investments.

She said New Zealand Super had some enormous benefits – including being simple, comprehensive and helped to reduce the degree of hardship amongst older people – but the problem was that people on high incomes were not being taxed enough.

“It would only really affect the top brackets, who wouldn’t even notice,” she said.

Pension researcher Michael Littlewood said while it was important to have a wider discussion about Super, current payment rates were sustainable. He said while most people would agree that we shouldn’t pay pensions to those who don’t need them, things were a bit more complicated than that.

“The trouble you get into though is where do you draw the line, where do you say our – that is the taxpayer – obligation to you finishes, or at least starts to finish, and where does it end altogether?

“Once you start putting a line in that particular income sand, you start having to make all sorts of judgements about what should count and shouldn’t.”

The Inland Revenue figures showed 2,500 people were getting Super payments while on incomes of more than $300,000. Littlewood said people would not give up that universal payment lightly.

“What do you think would happen if you put that line in the sand at 300k? Do you think that people would be entirely unresponsive to that? No, of course, they wouldn’t, they would shift their incomes around so their income was less than 300 (thousand dollars).”

Last year, NZ Super cost $14.5 billion and that cost is increasing by more than $1b each year. By 2024 it’s predicted to cost the country nearly $20b a year.

This piece was first published on RNZ.